What is Oracle Banking Payments (OBPM)?

Oracle Banking Payments (OBPM) is Oracle’s dedicated payments processing platform built to handle all types of bank payments — domestic, cross-border, high-value, retail, and real-time. It acts as a centralized payment hub that sits alongside FLEXCUBE Core, orchestrating how money moves in and out of a bank.

While FLEXCUBE Core manages accounts, customers, and balances, OBPM takes ownership of the payment lifecycle — from the moment a payment instruction is received, through validation, compliance screening, routing, and message generation, until final settlement and reconciliation.

Why Does a Bank Need a Dedicated Payments Engine?

Modern banks handle dozens of payment types across multiple rails — SWIFT for international wires, local RTGS and ACH systems for domestic transfers, SEPA in Europe, Faster Payments in the UK, UPI in India, and more. Each rail has its own message format, cut-off times, routing rules, and compliance requirements.

OBPM centralizes this complexity into one platform with a unified processing engine, reducing the risk of errors, duplication, and compliance gaps. It also provides a single audit trail across all payment types, which is critical for regulatory reporting.

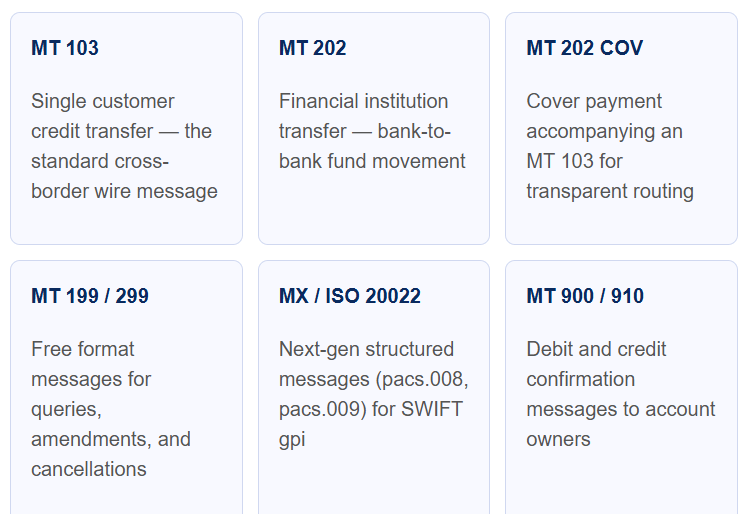

SWIFT Message Types Handled by OBPM

For cross-border payments, OBPM natively supports the SWIFT messaging network. Key message types include:

How a Cross-Border SWIFT Wire Flows Through OBPM

Below is the complete end-to-end journey of a customer-initiated cross-border payment through OBPM, from instruction to final settlement:

1 Payment instruction received

Customer submits a wire transfer request via branch, internet banking, or corporate portal. OBPM receives the instruction with beneficiary details, amount, currency, and value date.

Channel input

2 Validation & enrichment

OBPM validates the BIC code, IBAN format, account status, and available balance. It enriches the payment with correspondent bank details and resolves the routing — direct or via intermediary banks.

OBPM processing

3 Compliance screening

The payment is screened against sanctions lists (OFAC, UN, EU) and AML rules. If flagged, it is held for manual review. OBPM integrates with Oracle Financial Services Compliance or third-party screening engines.

Sanctions & AML

4 Charge calculation & FX conversion

OBPM applies the applicable charge option (OUR / SHA / BEN) and, if currencies differ, fetches the exchange rate from FLEXCUBE Treasury or a connected rate feed. The debit amount is calculated and the customer account is debited.

Pricing & FX

5 SWIFT message generation

OBPM generates the MT 103 message — structured with sender, receiver, beneficiary, amount, currency, and remittance information — and transmits it to the SWIFT network via the bank’s SWIFT interface (Alliance Access or similar).

MT 103 / pacs.008

6 Correspondent bank routing

The SWIFT message travels through one or more correspondent banks (Nostro routing). If a cover payment is needed, OBPM also sends an MT 202 COV to fund the correspondent’s Nostro account before the value date.

Nostro / correspondent

7 Beneficiary credit & reconciliation

The receiving bank credits the beneficiary’s account. OBPM receives confirmation (MT 910) and updates the payment status to completed. The Nostro account is reconciled in FLEXCUBE Core against the statement received.

Settlement complete

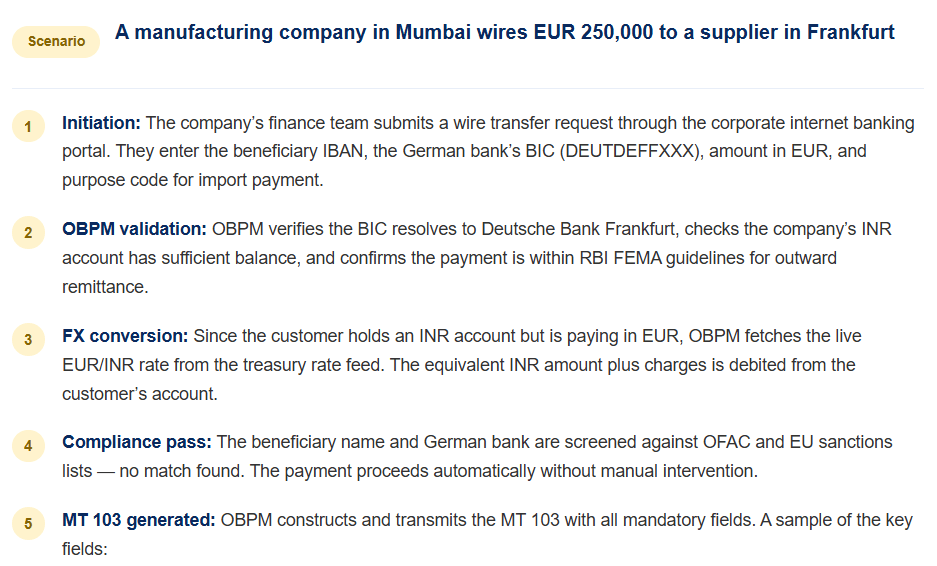

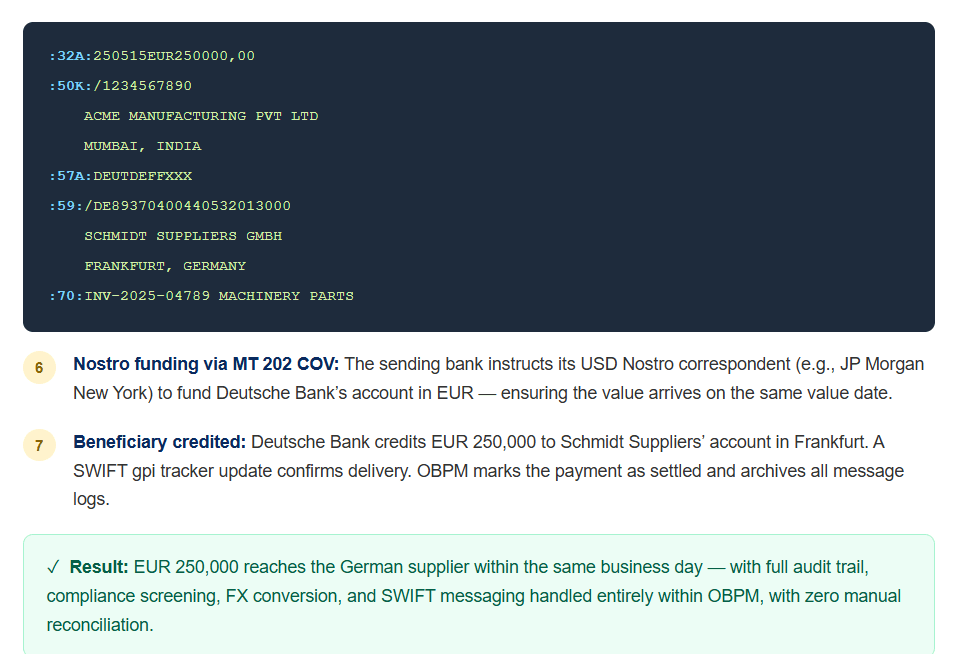

Real-World Use Case — An Indian Importer Paying a Supplier in Germany

Who Should Know OBPM?

Payments consultants Correspondent banking teams Trade finance operations Treasury & Nostro managers IT integrators Freshers in banking IT Testing & QA engineers

OBPM knowledge is highly valued in implementation projects — especially in banks migrating from legacy payment systems or adopting ISO 20022 for SWIFT compliance. It also connects directly to OBTF (Trade Finance) for document-backed payments and OBTR (Treasury) for FX rate feeds, making it a central component of the Oracle Banking ecosystem.

Leave a comment